Nigeria: Aiteo partners Mozambican firm Petromoc on 200,000bpd refinery

Almost all new supplies from Mozambique and Madagascar: China’s graphite imports are now up 2000% over the last ~18 months

5:07 CAT | 25 Jul 2019

China continues to increase its imports of natural graphite to meet rising domestic demand from the lithium-ion battery sector, with monthly imports increasing by 2,000% since the end of 2017 (before which they were less than 1ktpy) to exceed 22kt in May 2019. These figures exclude the import of very low value, crude material from North Korea. Almost all of the new shipments have come from Mozambique and Madagascar, where a large amount of new supply is becoming available.

China continues to ramp up natural graphite imports to meet rising domestic demand from its lithium-ion battery sector.

According to Roskill, monthly imports are now up 2000 per cent since the end of 2017, with almost all new shipments coming from Mozambique and Madagascar.

Prior to the end of 2017 China imported less than 1000 tonnes a year. In May 2019 imports exceeded 22,000t.

China has significant resources of battery-grade graphite, Roskill says, but many of the deposits being exploited are getting deeper and more expensive to mine.

“Coupled with rising environmental costs and other costs of production, China is looking increasingly to foreign sources of supply, in particular, those in Africa,” Roskill says. “. Almost all of the new shipments have come from Mozambique and Madagascar, where a large amount of new supply is becoming available.”

In 2017, Western graphite’s own ‘tip of the spear’ Syrah Resources (ASX:SYR) began production at its large-scale Balama project in Mozambique.

The miner, which is still having trouble hitting production targets, ships most of its graphite into the Chinese battery industry.

“Syrah Resources began production at its large-scale Balama flake graphite project in Mozambique in late 2017 and ramped up to more than 104kt of production in 2018; the vast majority of its shipments have been destined for the Chinese battery industry, ” reads the Roskill report.

Triton Minerals (ASX:TON) is also aiming to get the Ancuabe graphite project in Mozambique up and running in late 2020.

In Madagascar, several companies are looking to ramp up production of flake graphite, including Bass Metals (ASX:BSM) and Blackearth Minerals (ASX:BEM).

Tanzania is also a real hotbed of ASX-listed graphite development, with players like Graphex Mining (ASX:GPX), Black Rock Mining (ASX:BKT), Kibaran Resources (ASX:KNL), Volt Resources (ASX:VRC) and Magnis Energy Technologies (ASX:MNS) all moving projects toward first production.

In June, David Christensen, boss of Australian based Renascor Resources (ASX:RNU), told Stockhead there was a “paradigm shift” happening where there won’t be enough graphite, either synthetic or natural, for the growing lithium-ion battery market.

“The demand is the growing use of graphite in lithium-ion batteries, whether it is synthetic or natural flake, and we’re reaching a tipping point,” he says.

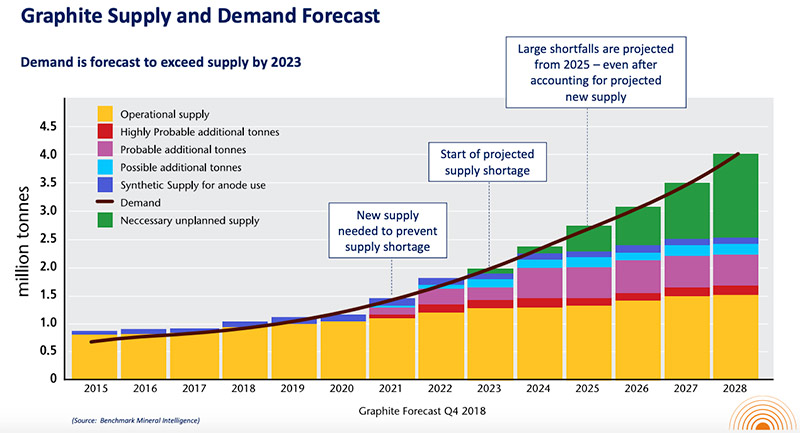

“By 2021 it looks like the natural flake graphite market will be in slight undersupply, even with new projected supply from sources like Syrah, but by 2023 that becomes quite acute.”

By Reuben Adams / Stockhead

Source: Stockhead /Roskill

Show comments

Also read

Leave a Reply

Be the First to Comment!

You must be logged in to post a comment.

You must be logged in to post a comment.